Introduction:

In Singapore, responsible financial management is crucial, especially when borrowing from Licensed Moneylenders. The Moneylender Credit Bureau (MLCB) plays a significant role in helping borrowers track and manage their credit history. This article provides a summary of frequently asked questions (FAQs) regarding the borrower’s credit report from the MLCB.

FAQ Summary:

1. Is It Necessary to Purchase My Own Loan Information Report?

No, it’s not necessary. Moneylenders typically purchase your Loan Information Report themselves when assessing your loan application.

2. How Can I Improve My Credit Standing?

To enhance your credit standing: Repay outstanding loans on time.

Keep the number of loans and total loan amount manageable within your financial means.

3. How Can I Access My Loan Information Report?

You can retrieve your Loan Information Report through these channels:

Online: Visit the MLCB website for immediate access.

In Person:

Visit MLCB’s office at 2 Shenton Way, #20-02, SGX Centre 1 Singapore 068804 for direct purchase (cash only).

Credit Counselling Singapore (Channel Partner): Visit CCS at 51 Cuppage Road, #07-06, Singapore 229469 to process the purchase.

4. What Is the Cost of Obtaining a Loan Information Report?

The cost is SGD 0.50 (GST inclusive) for a Loan Information Report.

5. Does the Loan Information Report Reflect Guarantor’s Responsibility?

Yes, the report reflects the guarantor or surety’s legal responsibility for any outstanding loans.

6. Is Information from Other Moneylenders Included in the Report?

Yes, Licensed Moneylenders refer to your most updated borrower’s credit report to assess if you’ve taken loans from other Licensed Moneylenders.

7. Are Approved-in-Principle Loans Included in Outstanding Principal Amount?

Yes, these loans are included while awaiting final approval. If you were only loan shopping, inform the lender to reject your application for an immediate update.

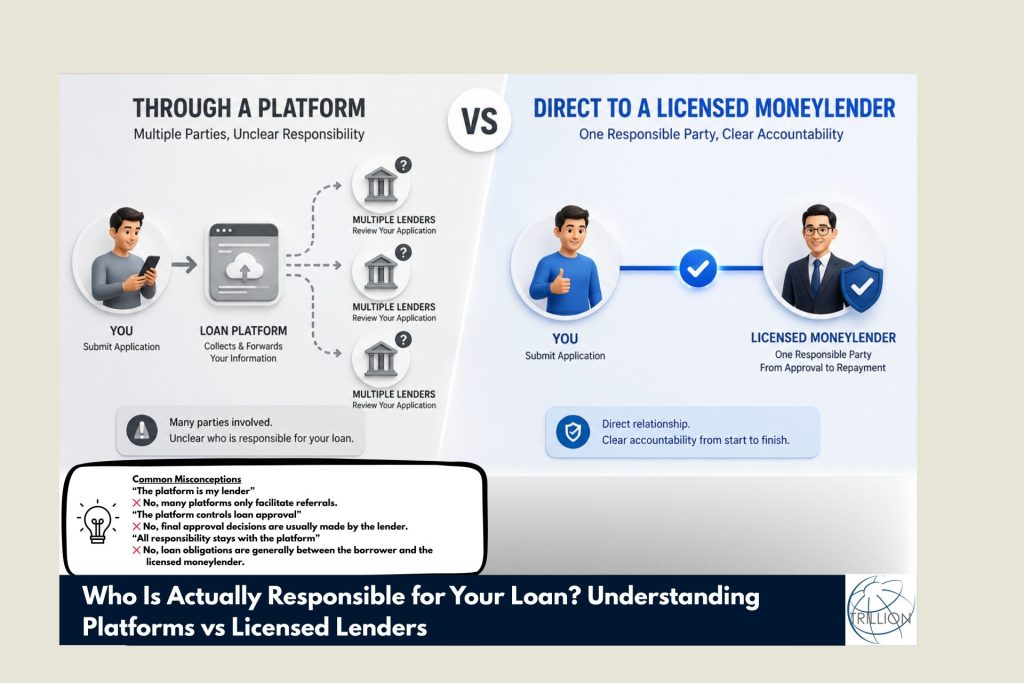

8. Who Decides on Loan Application Approval or Rejection?

The respective Licensed Moneylender makes the decision.

9. Can I Get More Information About Borrowing from Licensed Moneylenders?

Yes, borrowers can find additional details in the “Guide to Borrowing from Licensed Moneylenders” provided by the Registry of Moneylenders https://rom.mlaw.gov.sg/information-for-borrowers/guide-to-borrowing-from-licensed-moneylenders-english/

10. Does the Loan Information Report include any Bank loans or Credit Card Transactions?

No, it only includes loan and repayment information from Singapore’s Licensed Moneylenders.

11. How Can I Verify if a Moneylender Is Licensed in Singapore?

You can verify the license status of a moneylender by checking the official list of Licensed Moneylenders on the Registry of Moneylender’s website https://rom.mlaw.gov.sg/information-for-borrowers/list-of-licensed-moneylenders-in-singapore/

Conclusion:

Understanding your credit report from the Moneylender Credit Bureau is essential for responsible borrowing in Singapore. It helps you track your loan history, make informed financial decisions, and improve your credit standing.

Whether you’re applying for a loan or managing your existing debts, having access to this information empowers you to take control of your financial well-being.

{kind=link}

{kind=link}

{kind=link}