Introduction

In Singapore, more borrowers are applying for loans through online loan comparison platforms.

These platforms promote convenience by allowing users to:

Submit one application

Compare multiple lenders

Receive loan offers quickly

However, many borrowers overlook an important question:

👉 Who is actually responsible for your loan?

Is it:

The platform that collected your application?

Or the licensed moneylender providing the funds?

Understanding the difference is important because it affects:

Communication

Accountability

Repayment issues

Dispute handling

Overall borrower experience

In this guide, we explain how loan responsibility works in Singapore and why borrowers should understand who they are really dealing with.

Understanding the Difference Between Platforms and Lenders

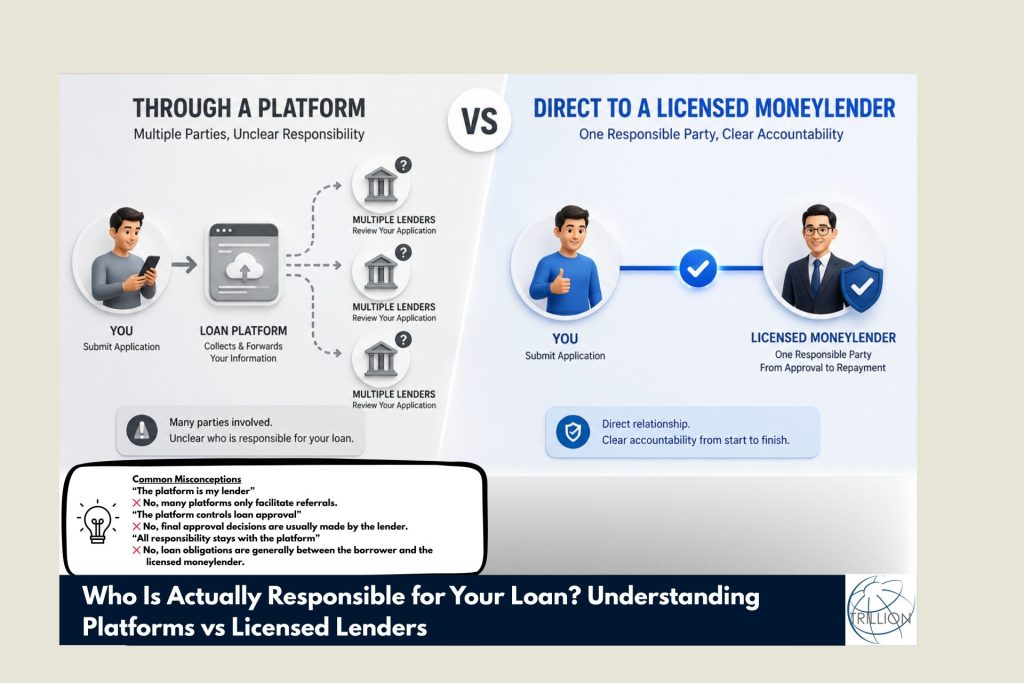

What Is a Loan Platform?

A loan platform generally acts as:

A referral intermediary

A lead-generation service

A comparison website

Its role is usually to:

Collect your application

Match you with participating lenders

Facilitate introductions

In most cases:

👉 The platform itself does not issue the loan.

What Is a Licensed Moneylender?

A licensed moneylender is the company legally authorised to:

Approve the loan

Issue the loan contract

Disburse the funds

Manage repayments

Licensed moneylenders in Singapore are regulated by the Registry of Moneylenders under the Ministry of Law Singapore through the Moneylenders Act.

So, Who Is Responsible for the Loan?

The Licensed Moneylender

The licensed moneylender is generally responsible for:

Loan approval decisions

Interest rates and fees

Contract terms

Loan disbursement

Repayment administration

Regulatory compliance

Once you sign the loan agreement:

👉 Your legal relationship is primarily with the lender.

What Role Does the Platform Play?

The platform’s involvement is usually limited to:

Collecting your application

Forwarding your information

Connecting you with lenders

After the referral stage:

👉 The licensed lender typically takes over the borrowing process.

This is why borrowers should understand:

Who the actual lender is

Which company is issuing the contract

Who to contact for loan-related matters

Why Accountability Matters

Many borrowers only think about accountability when issues arise.

For example:

Clarifying repayment terms

Requesting payment arrangements

Resolving disputes

Updating personal information

Handling repayment difficulties

In such situations:

👉 Knowing who is directly responsible becomes extremely important.

Communication Differences: Platform vs Direct Lender

Through a Loan Platform

Communication may involve:

Multiple parties

Different lender representatives

This can sometimes create:

Delays

Repeated explanations of your situation

Directly With a Licensed Moneylender

Applying directly usually provides:

Faster responses

Direct handling of questions and concerns

For many borrowers, this creates a more straightforward experience.

What About Loan Terms and Conditions?

Some borrowers mistakenly believe:

👉 The platform determines the loan terms.

In reality:

Interest rates

Repayment schedules

Fees and charges

Approval decisions

are generally determined by the licensed moneylender.

This is why it is important to:

✅ Read the loan contract carefully

✅ Verify the lender’s identity

✅ Understand who is issuing the loan

Data Sharing Considerations

When using a loan platform:

Your application may be distributed to multiple lenders within the platform’s network

This may result in:

Multiple follow-ups

Wider sharing of personal information

By contrast, applying directly typically means:

👉 Your data is submitted to only one lending company.

Why Some Borrowers Prefer Applying Directly

Many borrowers choose direct applications because they value:

Privacy

Faster communication

Direct accountability

Instead of dealing with intermediaries, they communicate directly with the lender handling the loan.

Questions Borrowers Should Ask Before Applying

Before submitting your application, ask:

Who is the actual lender?

Who approves the loan?

Who manages repayments?

Who should I contact if issues arise?

Will my information be shared with multiple companies?

These questions help avoid confusion later.

Common Misconceptions

“The platform is my lender”

❌ No, many platforms only facilitate referrals.

“The platform controls loan approval”

❌ No, final approval decisions are usually made by the lender.

“All responsibility stays with the platform”

❌ No, loan obligations are generally between the borrower and the licensed moneylender.

Final Thoughts

Loan platforms and licensed moneylenders serve different functions in Singapore’s lending ecosystem.

While platforms provide convenience and comparisons, the licensed moneylender is usually the party responsible for:

The loan contract

Loan servicing

Regulatory compliance

Repayment management

Understanding this distinction helps borrowers:

Make informed decisions

Know who they are dealing with

Avoid confusion during the borrowing process

For borrowers who prefer:

Direct communication

Clear accountability

Faster responses

👉 Applying directly with a licensed moneylender may provide a simpler and more transparent experience.

✅ Call to Action

Want a more direct and transparent borrowing experience?

Apply directly with professional licensed moneylender Trillion Credit in Singapore today and communicate directly with the company responsible for your loan from start to finish.

Walk into our branch or apply online anytime.

We’re here to provide fast, transparent, and legal cash loans — even on weekends.

📱 Call us at 65090111

📝 Or apply now at https://trillioncredit.com.sg/apply-for-loan/

✅ Frequently Asked Questions

Does a loan platform approve my loan?

Usually no. Loan approval decisions are typically made by the lender.

Can I contact the lender directly?

Yes. Borrowers should always know which licensed moneylender is handling their loan.

Is it better to apply directly?

You may apply directly if you prefer clearer communication, privacy, and accountability.

{kind=link}

{kind=link}

{kind=link}