Introduction

Loan comparison platforms have become increasingly popular in Singapore.

Many borrowers are attracted by promises such as:

“Compare multiple loans instantly”

“One application for many lenders”

“Fast approvals with minimal effort”

But an important question often gets overlooked:

👉 Are loan comparison platforms regulated the same way as licensed moneylenders in Singapore?

The answer is:

❌ Not exactly.

While licensed moneylenders operate under strict legal regulations, loan comparison platforms generally function under a different business model.

Understanding this distinction is important because it affects:

Accountability

Data handling

Borrower expectations

The overall loan application process

In this guide, we explain the differences clearly and simply.

What Is a Licensed Moneylender?

A licensed moneylender is a company legally authorised to provide loans in Singapore.

Licensed moneylenders are regulated by the Registry of Moneylenders under the Ministry of Law Singapore by the Moneylenders Act.

They must comply with rules relating to:

Interest rate limits

Fees and charges

Loan contracts

Borrower verification

Collection practices

Advertising restrictions

When you borrow directly from a licensed moneylender:

👉 The lender is responsible for issuing and managing the loan.

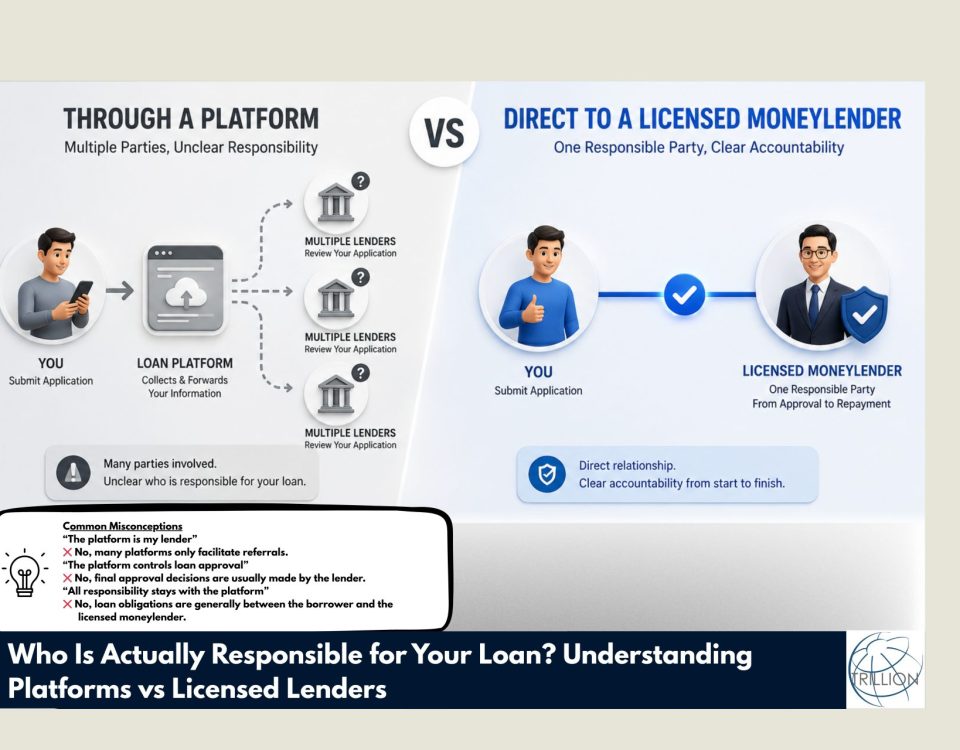

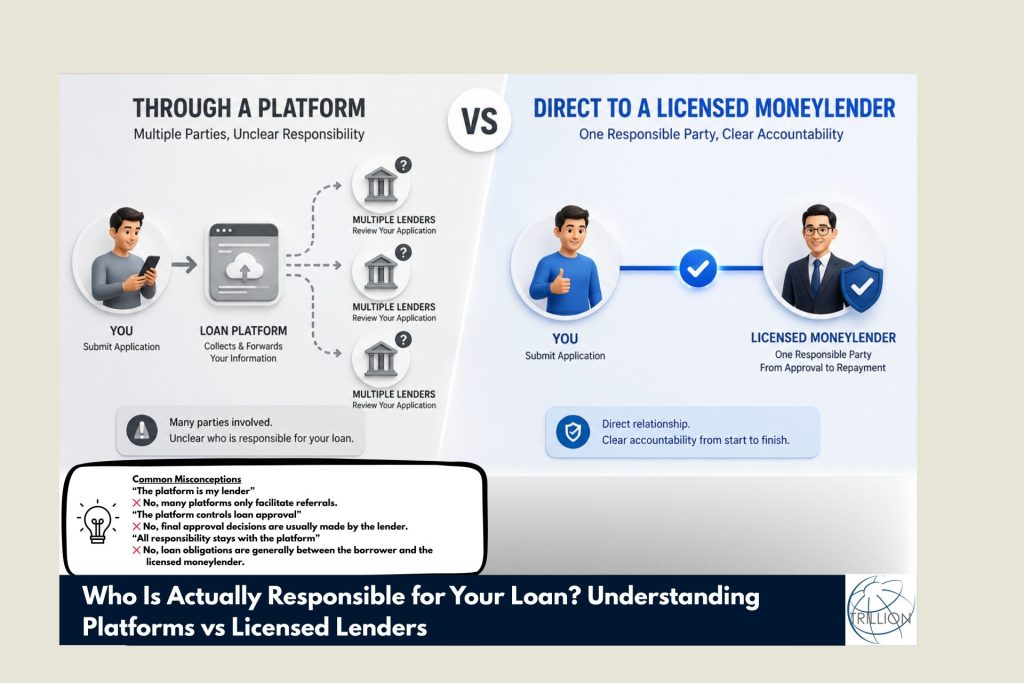

What Is a Loan Comparison Platform?

A loan comparison platform is typically a lead-generation or referral business.

Instead of lending money directly, these platforms usually:

Collect borrower applications

Match users with lenders

Refer leads to participating financial companies

Their revenue often comes from:

Referral commissions

Lead-generation arrangements

Marketing partnerships

This means:

👉 The platform itself is usually not the company issuing the loan.

So, Are Loan Platforms Regulated the Same Way?

The Short Answer: No

Licensed moneylenders are specifically regulated as lending businesses under Singapore’s moneylending laws.

Loan comparison platforms, however, generally operate as:

Marketing businesses

Referral intermediaries

Lead aggregators

As a result:

👉 They are not subject to the same operational regulations imposed on licensed moneylenders.

Why This Difference Matters to Borrowers

Many borrowers mistakenly assume:

The platform is the lender

The platform controls loan approval

The platform is directly responsible for loan terms

In reality:

👉 The actual loan contract is usually between the borrower and the licensed moneylender.

This distinction becomes important when dealing with:

Loan disputes

Clarification of terms

Repayment issues

Data privacy concerns

Who Is Responsible for the Loan?

Licensed Moneylender

The lender is responsible for:

Loan approval

Interest rates and fees

Contract terms

Repayment management

Compliance with moneylending regulations

Loan Comparison Platform

The platform generally facilitates:

Application collection

Matching services

Referral coordination

The platform may not:

Approve the loan directly

Control final loan terms

Manage repayment obligations

What Happens to Your Information?

When applying through a loan comparison platform:

Your details may be shared with multiple lenders within the platform’s network

This can sometimes lead to:

Multiple follow-ups

Privacy concerns

By contrast, applying directly to a licensed moneylender usually means:

👉 Your information is submitted to a single lending company only.

For borrowers who value privacy and control, this can be an important consideration.

Does Using a Platform Guarantee Approval?

Not necessarily.

Loan approval still depends on:

Income assessment

Existing financial obligations

Credit evaluation

Internal lender credit policies

A platform may increase the number of lenders reviewing your application, but:

❌ It does not guarantee approval.

Why Some Borrowers Use Loan Platforms

Loan platforms can be useful for:

Comparing multiple options quickly

Exploring lenders for the first time

Understanding general market offerings

For some borrowers, convenience is the main advantage.

Why Others Prefer Applying Directly

Other borrowers choose direct applications because they prefer:

Faster communication

Clearer accountability

More personalised assessment

Greater control over their information

Applying directly also reduces the number of intermediaries involved in the process.

Questions Borrowers Should Ask Before Applying

Before submitting any application, ask:

Who is the actual lender?

How will my data be used?

Will my application be shared with too many parties?

Who is responsible for the loan agreement?

Understanding these points helps borrowers make more informed decisions.

Final Thoughts

Loan comparison platforms and licensed moneylenders serve different roles in Singapore’s licensed moneylending ecosystem.

While such platforms provide convenience and comparisons, licensed moneylenders may be the entities directly regulated to issue and manage loans.

Understanding this distinction helps borrowers:

Know who they are dealing with

Make safer borrowing decisions

Choose the application process that best fits their needs

For borrowers who prioritise:

Direct communication

Transparency

Privacy

Faster processing

👉 Applying directly with a licensed moneylender may offer a more straightforward experience.

✅ Call to Action

Prefer a direct and transparent loan process?

Apply directly with professional licensed moneylender Trillion Credit in Singapore today and receive clear communication, structured loan terms, and a personalised assessment without unnecessary intermediaries.

Walk into our branch or apply online anytime.

We’re here to provide fast, transparent, and legal cash loans — even on weekends.

📱 Call us at 65090111

📝 Or apply now at https://trillioncredit.com.sg/apply-for-loan/

✅ Frequently Asked Questions

Are loan platforms regulated like licensed moneylenders?

No. Licensed moneylenders are specifically regulated under Singapore’s moneylending laws, while platforms usually operate under a different business model.

Who issues the actual loan?

The licensed moneylender—not the comparison platform—typically issues the loan contract.

Is it safer to apply directly?

Many borrowers prefer direct applications for clearer communication, greater privacy, and more direct accountability.

{kind=link}

{kind=link}

{kind=link}