Securing financing can be a game-changer for any small or medium enterprise (SME) in Singapore. Yet, many business owners face a frustrating hurdle: bank loan rejection.

If your application for a business loan has been denied, you’re not alone. Traditional banks often apply rigid criteria that many SMEs — especially younger or fast-growing ones — struggle to meet.

In this article, we explore the top 7 reasons banks reject SME loan applications in Singapore, and how you can avoid these pitfalls or consider alternative financing options like licensed moneylender business loans.

🚫 1. Limited or No Financial History

Many SMEs — especially startups and newly incorporated companies — don’t have a long financial track record.

Why banks reject:

Banks typically require 2-3 years of financial statements, including profit & loss accounts, balance sheets, and cash flow statements.

What you can do:

If you’re a newer business, consider financing options that don’t demand long financial histories — such as flexible SME loans from licensed moneylenders, who assess eligibility based on current revenue, director background, and operational needs.

🚫 2. Poor or Low Credit Scores

Your company’s credit score — or the personal credit score of directors — plays a big role in bank loan approvals.

Why banks reject:

Poor repayment history, late payments, or multiple existing loans can lower your chances.

What you can do:

Review your company and personal credit reports before applying. Clear any overdue debts if possible. If time-sensitive, choose licensed moneylenders who offer credit-friendly SME loans.

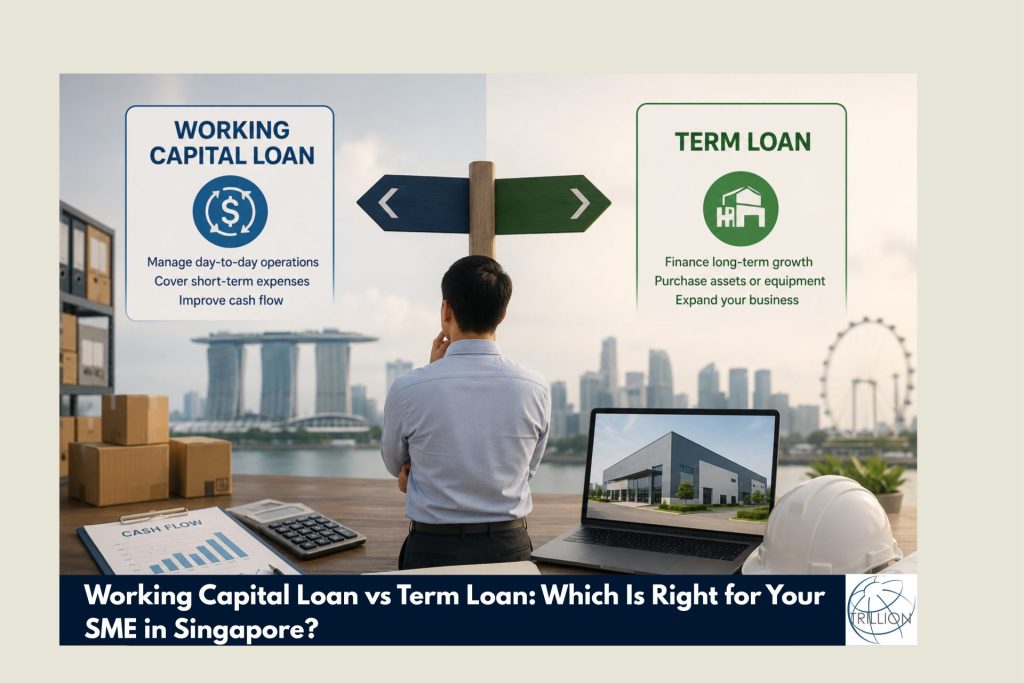

🚫 3. High Debt-to-Income Ratio

Banks assess how much of your revenue is already going toward repaying debts.

Why banks reject:

If your business is already servicing large loans, new borrowing is seen as high risk.

What you can do:

Consolidate existing debts or negotiate extended repayment periods. Or, look for working capital loans from licensed moneylenders, which are structured to work around such constraints.

🚫 4. Incomplete or Inaccurate Documentation

Missing documents or inconsistencies in your application can lead to immediate rejection.

Why banks reject:

Incorrect ACRA records, outdated financials, or incomplete forms are common red flags.

What you can do:

Always double-check application forms. If you’re unsure of what’s needed, opt for alternative licensed moneylenders who require less paperwork and offer guidance through the process.

🚫 5. Weak Cash Flow or Unstable Revenue

A profitable business on paper may still get rejected if monthly cash flow is irregular.

Why banks reject:

Banks want to see strong, consistent income that covers loan repayment and business expenses.

What you can do:

If cash flow is uneven due to seasonal income or project-based work, consider short-term cash flow loans from licensed moneylenders who are experienced with such industries.

🚫 6. Industry Risk or Business Model Uncertainty

Some industries are considered “high-risk” by banks — including F&B, events, retail, or logistics.

Why banks reject:

Banks may view volatile industries as too uncertain, especially in post-pandemic conditions.

What you can do:

If your industry is deemed high-risk, seek alternative funding from licensed moneylenders who specialize in SME loans across a wide range of industries.

🚫 7. Lack of Collateral or Personal Guarantees

Traditional banks often require personal guarantees or assets to back the loan.

Why banks reject:

If you don’t have real estate, vehicles, or other collateral, banks may decline your application.

What you can do:

Many licensed moneylenders offer unsecured business loans — no collateral required, just responsible lending based on your ability to repay.

✅ What to Do If You’re Rejected by a Bank

Don’t give up. There are still legal, safe, and regulated options in Singapore for SME financing.

At Trillion Credit, we offer:

✔ Fast SME loan approvals (1–3 working days)

✔ Minimal paperwork

✔ Flexible repayment plans

✔ No need for perfect credit or long financials

✔ Licensed and regulated by the Ministry of Law

Whether you’ve been rejected or simply need faster access to funding — we’re here to support your business goals.

📞 Need Financing Help Now?

Let us help you move forward with a transparent, fast, and hassle-free SME loan.

📱 Call us at 65090111

📝 Or apply now at https://trillioncredit.com.sg/apply-for-loan/

{kind=link}